Tokenized stocks have seen tremendous momentum ever since gaining initial traction last year. Weekly transfer volume across all chains crossed $2 billion for the first time last week, landing at $2.2 billion.

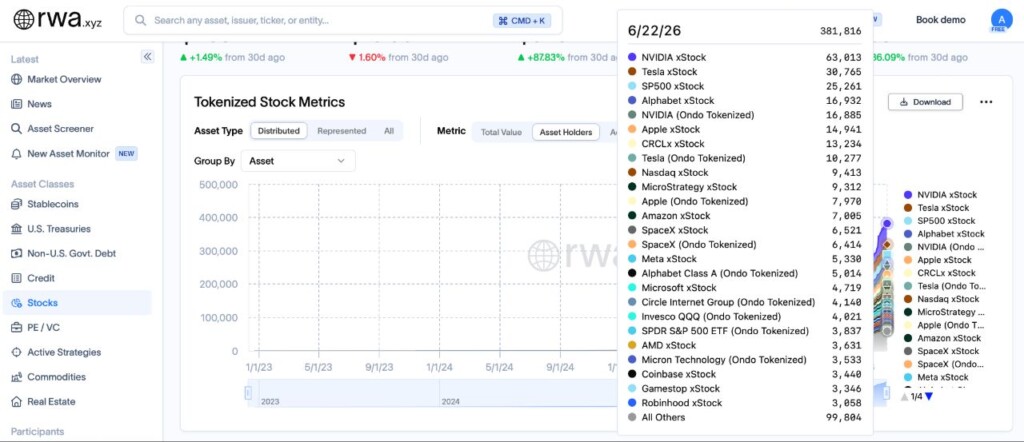

Apart from this throughput growth, the number of holders is another metric that has shot up in tandem. This number has tripled since January of this year. Tokenized stock holders went past 381,000 this week, a new high, up from roughly 122,000 at the start of the year, according to data from RWA.xyz.

Source: RWA.xyz

Accessibility is one of the main reasons why tokenized stocks have seen such growth over the past few months. Major wallet providers and centralized exchanges like Exodus, MetaMask, Phantom, Binance, Kraken and Robinhood EU now provide tokenized stocks right inside the apps. This effectively removes the friction for users across the globe to gain access on these platforms.

Clearer regulation also played a vital role in this growth story. The SEC’s May innovation exemption is poised to give issuers more room to operate, and Ondo secured approval across the EU and EEA.

The Volume Number Needs an Asterisk

It’s important to note that onchain transfer volume and retail trading are two different metrics. Transfer volume accounts for minting, redemptions and bridging between various networks. Therefore, transfer volume is a lot more than just buying and selling and the $2.2 billion mark can be seen as throughput. The tokens are being used, not just parked, but the figure overstates how much of that is someone clicking buy.

Scale is the other reality check. The entire tokenized stock sector sits around $1.4 billion. Set against global equities, that’s roughly 0.001%. Holdings stay concentrated in a handful of tickers, so a few names carry most of the weight.

The model also still cracks under pressure. In June, the SpaceX episode showed how fragile 1:1 backing gets when demand outruns supply. xStocks couldn’t secure the allocation it needed, and more than $1 billion was refunded across Binance, Bybit, Bitget and MEXC.

The Plumbing Is What Makes It Stick

The durability case isn’t in this week’s numbers. It’s in who is laying the rails. The DTCC, which clears most of America’s securities, is running a tokenization consortium. Broadridge is building onchain proxy voting, the unglamorous mechanics of shareholder rights. Franklin Templeton, a firm with real institutional weight, is already active in the space.

That’s the gap between a trend and a fixture. Retail flows can reverse inside a week. Settlement infrastructure built by the firms that already run traditional markets doesn’t unwind that easily. The $2.2 billion week grabs attention. The institutional groundwork is the reason the sector might still be standing when the next demand spike arrives.

The smartest crypto minds already read our newsletter. Want in? Join them.